Over the past decade, cryptocurrency has come a long way: first a marginal experiment, then a speculative asset, and now a fully-fledged instrument for investment and capital accumulation. Digital assets have firmly embedded themselves in the personal and corporate finances of hundreds of millions of people. However, there is still a systemic gap between owning cryptocurrency and actually using it within the everyday payment economy.

P2P conversion via exchange platforms means counterparty risk and operational delays. Bank transfers from crypto exchanges regularly trigger AML compliance, and accounts simply get frozen.

A virtual crypto card structurally closes this gap: it integrates crypto assets directly into traditional payment infrastructure, so you can use digital assets online and offline, anywhere in the world.

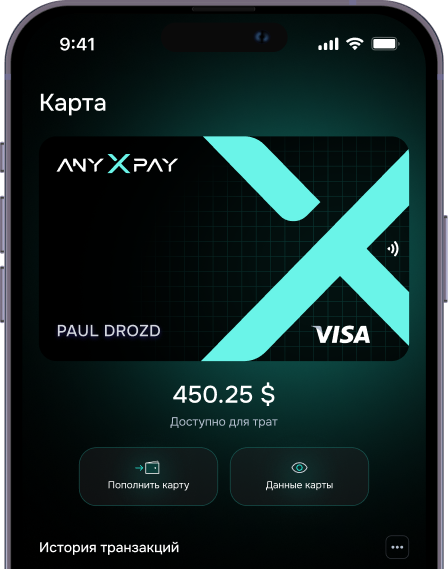

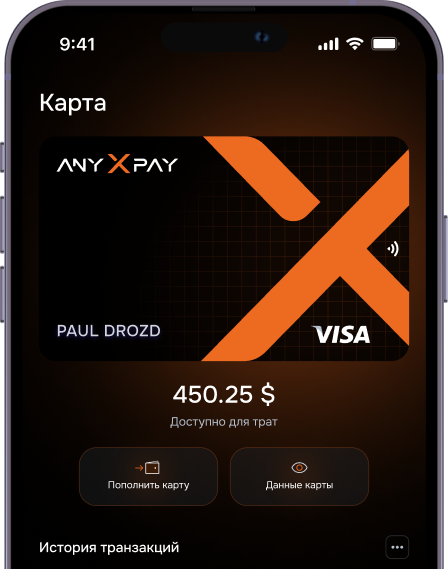

From a technical standpoint, a virtual crypto card is a Visa- or Mastercard-class payment instrument issued in digital form and functionally identical to a conventional bank card. It comes with a complete set of details: number, expiration date, CVV. It is compatible with Apple Pay and Google Pay and accepted anywhere card payment infrastructure is supported.

The key difference lies in how it is topped up. The user transfers cryptocurrency (USDT, BTC, ETH, and other supported assets) from a non-custodial wallet to the card balance: at this moment, conversion to fiat takes place, and the funds are credited in traditional currency. From there, the card operates like a regular bank product — a fiat balance, no additional conversions, no restrictions.

An important point: a virtual crypto card is not an investment or portfolio management tool. It is a consumption tool. It solves the last-mile problem — turning accumulated crypto capital into a liquid payment resource without having to go through the traditional banking system.

The global crypto economy has passed the point of no return. The total capitalization of the digital asset market consistently exceeds $2 trillion, and there are hundreds of millions of active cryptocurrency users. Crypto assets are integrated into corporate treasuries and used for international settlements and paying out compensation to distributed teams.

At the same time, infrastructure for consumer use of cryptocurrencies has historically lagged behind the market. Early crypto cards meant a high barrier to entry: multi-level KYC procedures, long verification, restrictive transaction limits, and an unstable operational environment. All of this created real barriers to mass adoption.

In 2026, the market offers something different. Here are three scenarios where a crypto card clearly outperforms the alternatives:

The crypto card market is saturated with offerings, but product quality varies significantly. Most users run into three systemic problems: excessive KYC requirements disproportionate to actual needs; tightening regulatory policy in various countries; and a fragmented user experience that requires a pile of additional apps.

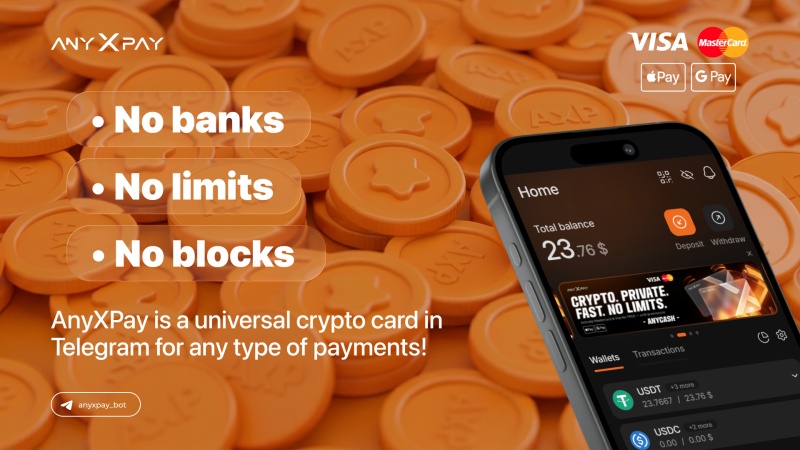

This is exactly what AnyXPay solves:

– Proportional verification. A simplified KYC procedure for the basic access level, with the option to extend verification for high-volume transactions.

– Security and reliability. Cards are issued through a network of independent issuers. If one partner comes under regulatory pressure, the system automatically switches to others. Funds are stored in cold wallets, with multi-layered anti-phishing protection in place.

– Operational integration. The card is issued and managed directly inside Telegram — no additional software to install and no new interface to learn. The wallet supports the major blockchain networks, and the card balance is denominated in US dollars.

A virtual crypto card does not compete with investment instruments — it complements them. Its function is fundamentally different: it closes the financial loop by turning accumulated crypto capital into a liquid resource that can be spent within the global infrastructure of traditional payments.

Cryptocurrency has gone from being an investment instrument to a full-fledged means of settlement. The next step is integration into the everyday payment economy without operational costs or jurisdictional barriers. That is exactly what AnyXPay does, built with maximum security and resilience as its top priority amid the strict regulatory environment of 2026.

The AnyXPay Telegram app is a completely non-custodial solution for your everyday transactions